The rise of artificial intelligence is not on the horizon.

It’s already here. Read Harvard Business Review, Forbes, The Conversation app, or any news post. As Peter H. Diamandis writes in Metatrend #2: AI & Quantum (2024), the question isn’t whether AI will change the world- it’s how quickly, and how well prepared we are to adapt. I’m a fan of his books.

Since 1997, I’ve worked with leaders across several sectors using the Action Learning model– a proven framework that aligns real-world problem-solving with strategic learning. In that time, I’ve watched leaders panic or pivot in the face of digital disruptions. You have seen the panic in 2008. Today is the pivot.

The key difference? Those leaders who thrive don’t wait for government programs or corporate re-skilling. They invest in mastering three core skills that shape their adaptability, agency, and long-term success. That’s why I earned my PhD in business psychology in my 50s… Here are some highlights. You can master these skills.

The Three Essential Skills in an AI World

In a recent Moonshots podcast conversation between Peter Diamandis and Tony Robbins, they outlined three core competencies to help leaders remain relevant:

Pattern Recognition, Pattern Utilization, and Pattern Creation.

These three skills are not new to those of us who practice Action Learning. In fact, they are embedded into the very DNA of our model.

Let’s break them down and show how they’re alive in the executive leaders I’ve coached for three decades. YOU can apply these three skills immediately.

1. Pattern Recognition: Learning from Data

Tony Robbins describes Pattern Recognition as the ability to look at history, human behavior, and technology trends and say, “I’ve seen this before.” The result is less fear.

In Action Learning, we often begin with what Revans called “programmed knowledge” and “questioning insight…” the act of recognizing patterns in current systems, processes, and outcomes. I teach leaders to ask questions like:

“Where else have you seen this behavior?”

“What patterns are repeating here?”

“What’s being ignored?”

“What numbers and words can we us to describe this behavior?”

For example: In a healthcare company facing massive turnover, our Action Learning team mapped resignation data and recognized patterns of burnout following project cycles. By naming the pattern, the client was no longer surprised by attrition. They recognized seasonality and then began to prevent it.

2. Pattern Utilization: Acting on What You See

Recognition is only useful if it leads to effective action. As Tony Robbins notes, civilization began when we learned to use the pattern of seasons—planting in spring, harvesting in fall. The leap from fear to control came through utilization. Today is the season of springtime.

In Action Learning, we emphasize “taking action and reflecting on the results.” A team that sees a pattern of client dissatisfaction, for example, must test new workflows, measure response times, before they can adapt. Tools like surveys, interviews, observations, 360 assessments are helpful.

For example: One healthcare client noticed repeated delays in patient discharges every Friday. Instead of managing around the bottleneck, they used Action Learning to test discharge protocol changes. They used cross functional teams, called Action Learning Sets, to explore solutions. They saw a 17% improvement in weekend flow within 60 days. And yes, automation helped immensely.

3. Pattern Creation: Designing What Comes Next

This is where great leaders shine. This is where YOU can shine.

Diamandis calls it the highest skill: creating new patterns. Not just responding to the world but reshaping it. He founded Singularity University, the XPrize’s, and the Open EXO community to embrace converging technologies. In Action Learning, we guide teams to generate new frameworks, policies, and cultural norms based on data and learning.

This level is visionary. It’s where leaders become creators. Practical creators of one solution after another.

For example:In a regional asphalt company, an Action Learning team created a new RACI-based scheduling protocol that reduced field crew conflicts by 42%. That new pattern, tested and refined by a newly promoted operations manager, became company policy within one quarter.

The BIG Identity Shift: From Manager to Creator

This AI revolution is not just about skills. It’s about identity.

The Action Learning model pushes leaders to shift from “problem manager” to “solution creator.” That’s the identity shift Robbins, Diamandis, Revans and I are describing. We say, “Stop managing problems. Start creating solutions.”

FACT 1: You won’t be replaced by AI. FACT 2: You’ll be replaced by someone who uses AI more creatively than you do… unless you become that person first.

If you’re interested in diving deeper into the frameworks behind this post:

Diamandis, Peter H. (2024). Metatrend #2: AI & Quantum.

Thank you for purchasing an authorized copy of this book and for complying with international copyright law. No part of this book may be reproduced or used in any manner without the prior written consent of the copyright owner, except for the use of brief quotations in a book review.

The information contained in this fictional book is not intended as a substitute for expert services or consultation with any financial, legal, or business consultants. All readers have unique circumstances that require specific expertise and customized solutions. All names included in this text are changed to protect the confidential identities of my clients.

Published by Gray Publications, a product of Action Learning Associates, LLC.

For book group study guide, consulting, speaking, bulk ordering information, or to request permissions, contact https://action-learning.com/ or www.Legacy-Locked.com at 3482 Stagecoach Drive, Franklin, TN, 37067, USA.

Paperback ISBN-13: 979-8-9900896-0-0 for $9.97 USD

Editing by Rob Hart at Reedsy

Cover design and interior formatting by eBookLaunch

Disclaimer: This fictional work contains complex characters who are more exciting than anyone ever met by the author… Hopefully readers will find their reflection in many of these characters and conflicts.

Chapters 1-5 introduce the three siblings, Will, Harper and Nora Lee Dawson, their setting in Nashville, TN, and urgency… The first advisor they hire is an attorney, named Jake Jr.

By 8:45 they met at a parking lot in 12 South. Will walked in silence beside his sisters. Rain pelted the sidewalks. His sisters huddled under a golf umbrella. He adjusted the hood of his raincoat.

He wondered, what the hell are we doing? Why are we meeting Harper’s old flame? Do we really need another lawyer in our lives? He repeated the family mantra like a drumbeat beneath the street noises: Protect our assets.

The building was full of steel and restraint.

A security guard in a tailored blazer confirmed their names and photo IDs. Then nodded them toward a shiny elevator. “First door on the right. Goes directly to the 15th floor. The top floor.”

Will gave a faint smile. At least someone in this town knows how to do their job.

“Do we need a game plan?” he asked.

Harper shrugged. “It’s called a Discovery Meeting. The point is to uncover what we don’t know.”

As the elevator climbed, Will caught their reflections in the brushed steel wall. He bit his tongue.

Three Dawsons. Blurred outlines. Unspoken tensions between them.

No script.

Not much trust.

Only a shared name and shared risks.

And somewhere above them, Jake Madducks Jr. waited.

With his shiny shoes and a view worth fighting for.

The elevator ride to the Madducks Law Firm felt like an ascent into something mythic.

Will stood between his sisters in the mirrored cab. Harper, poised and flawless as always, stared straight ahead. Nora Lee checked her phone, her thumb flicking through notes. Rain glistened on their jackets. The air smelled like wet wool and nerves.

“I think we need a game plan,” Will declared.

Harper didn’t look up. “It’s a discovery meeting. Which means we’ll talk. They’ll listen. And send a bill.”

They reached the top floor. The doors opened to a quiet lobby. All polished concrete and understated wealth. A single executive assistant escorted them to the office suite. She offered drinks but they were denied.

Will muttered, “So far, better than Chamberlain’s place.”

They stepped into an empty room.

Minutes later Jake Madducks Jr. sashayed in like he was walking on stage.

Yellow suitcoat. Green bowtie. White shirt too eager for starch. Shoes polished to a shine so sharp that Will squinted. He moved like someone who had practiced his entrance. Confidence wasn’t the best word. It was all theater.

“Greetings and such,” he bellowed. “Jake Madducks Jr., Counselor-at-Large. Welcome to all y’all.”

Harper hugged him slightly longer than required. Introductions followed.

Jake Jr. ushered them into his corner office. His sanctum. An explosion of leather, locked filing cabinets, polished boardroom table, and a panoramic view of Nashville’s ever-changing skyline. Downtown cranes perched like giants frozen mid-reach.

Will eyed the skyline. “Nice view.”

Jake Jr. winked. “Got to protect the important things.”

Will wondered. Should I let Harper lead this meeting? Should I grill this character? Take the long view? Maybe I should watch the cards fall on the table.

“Well of course I want to take care of all y’all,” Jake Jr. crooned. He used both hands to pull his hair up and over his head as he leaned back. “Please have a seat. Coffee? Sweet tea? No? Then how about if someone shares what brought you into my lovely office today?”

They got to business.

Harper started. “As you may recall, the Dawson family has significant assets in Williamson County. And two other regions. Each of us receives quarterly trust distributions. Those payments increased when we turned thirty. We’re not cash poor. That’s not the problem.”

Jake Jr. nodded. “So, what brings you in?”

“Our father died yesterday. Cardiac arrest. Suddenly.”

Jake Jr.’s eyebrows rose just enough.

“We meet on Friday with Chamberlain Law,” Will added. “Our parents’ firm. Tomorrow.”

“But we’ve never seen the legal documents,” Harper said. “Not the wills. Not the trust terms. Not even confirmation of trust officers.”

Jake Jr. leaned forward. “Do you know the size of those assets?”

Will’s tone was iron. “That’s not relevant here. Or to be shared.”

Jake Jr. raised his palms. “Understood. Let’s reframe: Do you have an asset map?”

Harper shook her head. “Problem #2.”

Jake Jr. clicked his pen. “So: estate documents missing, trust terms unknown, and no clear line of succession. You assume Chamberlain has something legally binding?”

Will said, “We do assume. We hope. But hope is never a strategy.”

Jake Jr. nodded thoughtfully. “That’s common. In wealthy families like yours, parents hold cards close. It’s part legacy. Part asset control. Parents often think of their adult children as little kids.”

Harper declared, “The Transfer on Death law is firm in Tennessee.”

“Yes,” said Jake Jr. “For good reason. Plenty of outsiders have stolen assets from too many of our neighbors. And family members. There are too few antebellum plantations left. A damn shame. Countless celebrities and wealthy people relocate to Tennessee just to avoid capital gains taxes. Too many damn Californians are buying up our lands. Just stating a fact. As you well know, we protect the celebrities in our town, for good reasons.”

Nora Lee added, “I keep a running list… Justin Timberlake and Jessica Biel. Nicole Kidman and Keith Urban. Carrie Underwood and Mike Fisher. Tim McGraw and Faith Hill…”

Will cut her off, “I’m not sure any of that is relevant.”

“Agreed. Then there’s Regan,” Harper said. “Our mother.”

Jake Jr. leaned forward. “And… what’s your concern?”

Harper paused and looked at Will. He asked, “Are we speaking in confidence?”

Jake Jr. declared, “Yes. Definitely. Attorney-client privilege extends to Discovery Sessions like this one. We always practice confidentiality here at Madducks Law. The day any attorney breaches that practice is the day they lose their credibility. And their reputation.”

Will kept wondering. Is reputation more important to you than anything? That yellow suitcoat screams louder than any billboard.

Harper continued. “In confidence, then, problem #3 is our mother, Regan. She keeps her cards close to her chest.”

“That’s a solid habit when playing poker at a table of hostiles. What’s the problem?”

Harper paused again. “Jake Jr., you may recall when we were in our study group you said that I was ruthless, right?”

“I think my words were a bit stronger. Something like, “you’re a ruthless son of a bitch.” He smiled.

“Yes. Well, our mother is the bitch. She bends the rules until she wins. She bluffs high and rarely folds her cards. She has no friends. Our father was her arm candy. He somehow tampered her down when she got too ruthless. And now he’s gone. We haven’t talked about her much, even between ourselves. She is intimidating.”

“She’s… a wild card,” Nora Lee said carefully. “She bends rules until they break.”

“She’s a closer,” Will said flatly. “Our father fronted the charm. She closed the deals.”

Jake Jr’s eyes flicked between them. “So, she’s likely to be named as the executor?”

“Problem #3,” Will said. “We don’t know. Could be her. Could be Chamberlain. Could be someone we’ve never met.”

Jake Jr. brushed his hair back with both hands and leaned back again. “That’s why you’re here.”

Harper nodded. “And because we don’t want to walk into tomorrow’s meeting blind.”

Jake Jr.’s tone shifted slightly. “If I understand, you’re seeking leverage. Legal or strategic. Before seeing documents that may define your future.”

Nora Lee said quietly, “We’re not trying to fight. We’re trying to understand.”

Jake Jr. softened. “Then let’s keep things simple.”

He rose, walked to the whiteboard, and began drawing three boxes.

Jake Jr. turned. “Here in Tennessee, if your father died intestate, your mother would receive a third of the estate. Or equal to one share if the split favors her. But if a valid will exists, everything depends on the executor and the trust language.”

“Problem is,” Harper said, “we don’t know which box we’re in. One. Two. Or three.”

“Not yet,” Jake Jr. agreed. “But we can start identifying who might hold that power.”

Will spoke loudly. “We’ve never been told anything. No succession talks. No planning. Just the family mantra: ‘Protect our assets. Trust nobody.’”

Jake Jr. smiled. “Sounds like your parents wanted survivors. Not stewards.”

Will didn’t smile back. “Maybe both.”

They all fell into silence. Nashville shimmered through the glass windows. Bright, ambitious, unfeeling.

Jake Jr. finally said, “Well, you’re here now. That’s a start.”

Jake Jr. brushed his hair back with both hands. Twice. Then he stood and faced them as if in a courtroom. “Yes. Yes of course. Tell me more about your mother.”

Will spoke loudly, “Frankly, she’s a reckless, greedy son of a bitch.”

Jake Jr. leaned forward, “Now you’re getting interesting.”

Will started, “Here’s an example. In confidence of course.”

“Of course,” said Jake Jr. “This meeting is not being recorded in any manner.”

Will began, “When we were teenagers our parents accelerated their real estate investments. They acquired properties and grew faster than Hobby Lobby. Another local family enterprise. But they never paid a fair market value. Even for our neighbors. They used the Smucker Firm to undervalue properties, based on fabricated risks. Water contamination. Toxic chemicals. Drainage. Undeclared easements. Mineral rights. Fake cemeteries. The details varied but the outcome was always the same.”

“It wasn’t always that drastic,” said Nora Lee. “They weren’t criminals or anything.”

“They skirted the laws,” said Harper. “That’s one reason why they never talked about business with us.”

“And one reason why Harper and I have never been involved. Somehow cut-throat real estate deals were not for young women to discuss,” said Nora Lee.

“Even though our mother, Regan, had a long history of being ruthless. You know about fact patterns. When there’s smoke everywhere, someone’s hiding a match,” said Harper.

Jake Jr. smiled again. “I like you three.”

“Let me give you some more context,” said Will. “When the Smucker Firm said that a property was worth 50% less than other appraisals, the sellers got scared. Every time. They ended up selling for 40% of their asking price. The sellers didn’t know any better. Most local sellers were farmers who inherited the land. Some were old church properties with deacons who were well intentioned but clueless. The sellers were astounded by the growth in Williamson County.”

“But they were told that if they didn’t accept the Dawson offer, then the Smucker Firm would make those risks public. Then the sellers would never see a better offer. Not quite extortion. Not quite illegal. And of course there were never any records of those private talks. But the fact pattern got back to me. Frankly, the three of us have never discussed how our parents acquired their assets.”

“Mostly because two of us, as girls or women, were shut out of the damned family business!” said Harper.

“Also, because I got scared,” said Nora Lee. “We were told to share our opinions. But if I did, I got shut down. So, I retreated. Part of me still doesn’t want to know how they gained so much wealth in only 30-40 years.”

“I can tell you that. I studied them,” said Will. “When needed, our mother was the closer. But most of the time she leveraged the Smucker Firm. They fabricated risks used as leverage to buy assets at reduced rates.”

Jake Jr. leaned forward. “Who owns the Smucker Firm?”

Will groaned. “I don’t know. The CEO is an empty suit. I’ve asked Chamberlain but the old bastard never answers me directly. Our father was the more friendly face in business. And our mother was the greedy son of a bitch. Behind the curtain unless needed.”

“Take it easy, Will,” said Nora Lee.

“Why? We haven’t talked about them. Maybe today is the day to do so! We’re all adults. This meeting is in confidence. Right?”

“Absolutely,” said Jake Jr. “And you three have a fascinating story. Do you have any examples with evidentiary material, like deeds or email threads?”

“Yes, of course,” said Will. “That has been my role for the past 10 years. I manage properties after they acquired them. Here’s an example that was described in the Williamson Herald. Plenty of local dispute from bloggers. The bottom line up front is that our mother always gets more reckless when the stakes get higher.”

“Easy bro,” Nora Lee spoke quietly.

“I think he needs to know some details! Context. We need to bring some of these stories to the surface,” said Will. “Hear me out then you can decide.”

“Discovery. That’s why we’re here,” said Harper.

Will continued. “One of our neighbors owned 520 acres of rolling farmland, just off Cool Spring Boulevard. Before the mall was created, we used to ride dirt bikes there. Bicycles. Not motorcycles. It was one of the largest parcels in Williamson County. And it was one of the only times when they had to use a personal line of credit from the bank. She wrote the demand letter and terms. His name was used. Not hers.”

“Yikes,” said Jake Jr.

“Exactly. He was furious with her! And her private accounts were transferred to First Citizens Bank. To establish some distance from his risks. She kept spending. Like any addicted gambler. He could express frustration. Or his fury. But he could never manage her.”

Harper spoke up, “So, now we are like those sellers. We think we have assets. But we don’t know their value. And we can’t access the papers. None of us want to be her next target. We want to know our options.”

Nora Lee whispered for the second time, “So, can you help us?”

Jake Jr. ran both hands through his hair. Three times. That gesture bought him time.

“Well,” he said, in that stretched Southern drawl, “yes of course I can help y’all. Be glad to. What a fascinating family you have.”

He paused like an actor waiting for the next cue. Then he walked to the head of the boardroom desk.

“We’ll start with the basics. Here in Tennessee, when someone dies without a valid will, that’s called dying intestate. Our laws dictate asset distribution. In your case…”

“Spouse and children,” Harper interrupted. “We know. The closest surviving relatives.”

Jake didn’t flinch. “Right. But legal structures don’t always match the deceased’s intentions. That’s why a valid will matters. Any documentation? Estate plan? Drafts?”

“No.” Will’s voice was hard. “That’s problem number one. Remember?”

Shit. Did you not hear us the first time? Another empty suit. A yellow suit coat. We’re wasting our time here…

Jake opened his arms like a preacher mid-sermon. “So! No copy of a will means we begin with assumptions. If your father left no valid document- and I’m not saying that’s certain- then the spouse receives either a third or an equal share with children. Whichever is greater.”

“Because there are three of you,” he continued, “that could mean your mother gets a quarter. The rest of the estate gets split evenly between you kids.”

“We just don’t know,” Harper snapped. “So, we assume the worst. That’s why we’re here.”

“I’m confused,” Nora Lee said. “You said ‘whichever is greater.’ So, is it a third, or a quarter?”

Jake gave a politician’s shrug. “Can’t say yet. Again, that’s assuming there’s not a will. A big if. Box number one.”

Nora Lee leaned in. “What about Emily? His first wife?”

“Divorced and remarried? Then no. She’s not in his intestate line, legally speaking.”

Will’s thoughts moved faster than the shifting wind in the room.

At least Jake didn’t say ‘It depends.’ But what is Nora Lee fishing for?

“Has she reached out to you?” Will asked her. “Emily texted me yesterday. I didn’t reply.”

Harper rolled her eyes. “She’s not relevant. Lonely. Maybe a gold digger. Keeps Dawson as her last name like some sad identity badge. Lives alone with her cats.”

Nora Lee paused then spoke quietly. “She never remarried. No kids. That’s true. But she wants to stay connected.”

Harper stared. “Something you want to share, sis?”

“Maybe. Maybe not. I like her. We talk. She cares about us. About all of us.”

Will stared at the floor.

So, Emily’s been meeting with our baby sister. Gathering intel. Why? Is she angling for something? Payments? Position? Did Emily and our father stay close after their divorce?

Jake Jr. shifted his feet- ready for a second boxing round. “Right. Second scenario: there may be legal documents, but none of you have access. Box number two. That limits your power. Without a will, you can’t execute your father’s intentions, whatever they were.”

Harper’s fists clenched. “So, we’re screwed? Damn it all.”

Jake Jr. kept calm. “You believe a valid will exists. But you don’t have a copy. So, we begin where the law begins. With assumptions. In the absence of a will, the state steps in. If there’s a surviving spouse and three children, like all y’all, then you each get a quarter.”

“Unless,” Harper said, “there’s a will that says something else.”

Jake Jr. nodded, lips pressed tight. “Exactly. And we don’t know that yet. So, worst-case scenario planning makes sense.”

“I still don’t understand,” Nora Lee said. “You said the spouse gets a third. Now it’s a quarter?”

Jake Jr. raised a finger. “It’s whichever is greater: a third, or an equal share with the kids. In your case, four potential heirs, so one-fourth to each. That’s if there’s no will. These are fictional examples.”

Harper leaned forward. “And if there is a will?”

“Then everything depends on what it says. The details. Executor named. Beneficiaries listed. Powers granted. If it even exists.”

Harper nodded, her voice sharp. “Which brings us back here.”

Will scratched his jaw. “And what about his first wife? Emily?”

“She’s not part of this,” Harper said quickly. “Divorced. No children. No claims.”

Nora Lee shifted in her chair. “That’s not entirely true. She never remarried. Kept the Dawson name. And she reaches out.”

Will watched Harper narrow her eyes. “Is there something we should know?”

Nora Lee hesitated. “We have tea. Every few months. She cares about the family reputation. She asks questions.”

Harper snorted. “Sounds like intel gathering.”

“She’s lonely,” Nora Lee said. “That’s not a crime.”

Will didn’t speak. But the thoughts were already formed.

Nora Lee’s too quiet. That always means something. I wonder if someone else has a copy of the estate documents. I wonder if Nora Lee has taken a copy from Emily.

Jake Jr. stepped forward again, his voice quickening.

“Now. Back to the second scenario: a legal will exists, but you don’t have access. That seems to be your reality.”

Harper’s voice cut clean. “So, what can we do?”

Jake Jr. didn’t sugarcoat it. “Very little. If you can’t produce the document, you can’t assert its contents. Hearsay doesn’t hold in probate court. No matter how many times your father may have said something over a bourbon.”

“And what if he said he wanted to exclude someone?” Will asked.

“Still hearsay,” Jake Jr. replied. “Intentions are not legal instructions.”

Harper swore under her breath. “So, now what? We’re screwed?”

Jake Jr. didn’t answer. He just kept moving. Literally pacing like a man boxing invisible shadows.

“Best case? Chamberlain Law has a clean will, sealed, signed, dated. Written in sound mind and body. With witnesses. Names an executor. Lists the assets. Designates power of distribution. Those legal responsibilities are clearly defined.”

He turned to the siblings. “Did your father name any of you executor?”

They exchanged glances. Pauses. Each shook their head sideways.

Will thought of the mantra. Trust nobody. That fact sucks. He didn’t name any of us. If our father didn’t trust me to manage the estate, what else didn’t he trust me with?

Jake Jr. punched forward. “If none of you are named, the next likely executor is your mother.”

Will exhaled through his nose. “Of course. Shit.”

“She’s experienced,” Jake Jr. added. “Business-savvy. Ruthless, maybe, but probably capable. Most surviving spouses are named as the executor. Even if that person is struggling with grief. That’s why survivors are targeted by wealth advisors and insurance salesmen. Damned vultures.”

Will muttered, “She’s capable of doing whatever the hell she wants.”

Jake Jr. let that sit.

Then he said, “There’s a third possibility. Box three. If your father named someone outside the family. A friend. A firm. To avoid infighting. Or legal disputes. Or manage philanthropy. It happens.”

Harper’s voice was cold and slow. “Topher Chamberlain, maybe?”

Jake Jr. didn’t respond. He couldn’t.

Will clenched his fists beneath the table.

“There’s also a fourth possibility,” Jake offered, warming again. “Extended family. Uncle, aunt, cousin. Someone who knows the internal dynamics but isn’t at the emotional epicenter. Someone who can manage a family foundation. That can be ideal in high-net worth estates.”

“We don’t have extended family like that,” Will said. “Thanksgiving is a very small event.”

Jake Jr. gave a half-shrug. “Still worth asking.”

Harper said, “Huh? What about a family foundation? We’ve never discussed one.”

Nora Lee broke her silence.

“There is a family foundation,” she said softly. “I’ve been running it for six years.”

The Dawson Family Foundation announces a new charter: focused on financial education, small business equity, and trauma recovery in Southern communities.

The board now includes all three Dawson siblings, with rotating leadership every two years. Plus, four independent board members with non-competing expertise.

A final clause stated, “We share the belief that leadership must evolve. Or it ceases to be effective.”

Back in Richard’s former office, two granite blocks sat on the Reliance oak desk.

The family motto had changed.

Will had engraved a new granite block with a brass plate and golden letters.

Protect our purpose. Trust each other.

Discussion Questions for your Book Club or family meeting:

1. About your family

When Richard Dawson, the family’s powerful patriarch dies without an estate plan, the heirs face a cascade of secrets, succession struggles, and long-buried grievances. For unexplained reasons, their mother Regan is absent. Loyalty is fragile. Memory is unreliable. Blood may not be thicker than paper… So, how is this plot similar or different from your family of origin? Your current family? Your desired family?

2. “Protect Our Assets. Trust Nobody”

These phrases repeat throughout the story like a heartbeat. How do they shape each characters’ behavior? Their relationships? Is it a legacy or a curse or something else…?

3. Family Identity and Roles

Each sibling (Will, Harper, Nora Lee) reacts differently to Richard’s death and Regan’s absence. They crave different things- stability, control, or peace. How are their roles shaped by birth order, gender, personality, or blind spots? What is unrealistic about their behavior? What characters do you relate to most, and why?

4. Inheritance and Power

The notion that adult siblings have no awareness of a $120 million inheritance is unrealistic. And not impossible. Would the story be less impactful of the inheritance was $1million or $10 million? What does inheritance mean in this story- money, control, memory, responsibility, or…? How do the siblings navigate entitlement vs. purpose? Dr. Jenn says, “Time is Right.” Do you agree?

5. Regret and Silence

Many characters- especially Will and Nora Lee- carry unspoken regrets. This story is only one week in their lives. What moments reveal their regrets and fears most clearly? Why do these silences persist?

6. Southern Setting and Expectations

How does the Nashville backdrop influence expectations for behavior, gender roles, and power dynamics in the family? How do the scenes in Monteagle contrast to the scenes at Hickory Ridge? How do the indoor and outdoor scenes contrast? How do music, food, guns, preppers, and religion influence these characters?

7. Emily and Regan

Compare the characters of Emily and Regan, two matriarchs with different legacies. And very different family roles. Matriarchs often lead family succession plans and wealth distribution. What do their choices say about survival, visibility, and emotional costs in this family system?

8. Real Psychology, Real Stakes

The author is a behavioral psychologist. (Some useful definitions are provided in the next pages for your reference.) Where do you see real-life psychology reflected in these characters’ decisions? Do the siblings develop psychological capital? How does their advisor triad (Dr. Jenn- process, Colton- wealth, Jake Jr.- legal) accelerate their behavior changes?

9. Bonus Question

What would you do if you discovered your family had no succession plan- but millions in assets and secret enemies within?

Some Useful Definitions with examples:

Active listening = a communication practice that requires sharing information until the speaker feels validated. Example: When Nora Lee asked, “Did he ever say he was proud of us?” and Will didn’t rush to answer. That was active listening. The kind that leaves space for reflection or truth.

Active owners = people with voting shares of an asset, including risks or rewards

Advisory board = a group of trusted advisors who provide advice to owners

Agency = an individual’s capacity to state important thoughts or feelings. Examples: Harper finally called a new legal team at Madducks Law. That wasn’t rebellion. It was agency, and perhaps long overdue. Will texted Dr. Jenn, and then Colton, and added them to the advisor team. Nora Lee reached out to Hannah, ventured beyond D-House, and brought a surprise guest musician to the Hickory Ridge dinner. Agency describes each character’s development.

Aspirational goal = a big, unattainable vision of a better future

Aspirational behavior = an exceptional, remarkable behavior from people who exceed expectations

Behavioral script = a communication model used to state feelings, undesired behavior, and desirable behavior

Business system = a description of how people fit into a unique system and deliver a valuable product or service

Complete communication wheel = a script with five parts: data, emotion, judgment, want, will, plus opening and closing questions

Conflict = a response to different data or perspectives. One conflict model describes the interactions between task, relationship and process. Example: The siblings have more relationship conflict than task conflict. They don’t disagree about money, because they don’t know much about money. But when Harper needed to fight for her son, Mason, all the characters quickly responded to that conflict!

Conflict management = the process of responding to others with degrees of assertiveness or cooperation

Constructive feedback =positive statements that focus on desired, prosocial behaviors

Culture = a model used to describe organizations, based on underlying assumptions, stated values and artifacts

Data = facts that are quantitative (using numbers) or qualitative (using images or words). Example: The distribution decisions are reversed to make some points about data. These siblings do not approve their parent’s distributions in G&G. They do approve of the distributions to themselves, the family foundation, and the well-being trusts. Those are each data points, facts.

Destructive feedback = negative statements that diminish others, and should be avoided.

Distributions = financial or equity assets that are managed and transferred over time. Examples: The Dawson siblings have had distributions for years. As Harper says, “We are not cash poor.” Their frustrations about distributions include the mysterious terms of the trust officers, location of the estate documents, and scope. They learn to trust Chamberlain. But they don’t have a clue about stewardship or future distributions.

Empathy = the capacity to understand another person’s perspective

External audit = an assessment process led by expert financial, legal or talent consultants

Family system = a description of how related people support their shared values and beliefs

Family capital = a dynamic social construct of shared values lived intentionally. Example: When Dr. Jenn introduces this term, the siblings realize that they have family capital. That it can change. That they need to be intentional together, to protect their inheritance and legacy.

Feedback =what others say or do that shapes personal learning

Fiduciary board = a group of expert advisors with financial responsibility for an asset

Fixed mindset = a belief opposing new ideas or behavior

Flow optimization = a behavioral model describing the balance between challenge and skill

Formal learning = the process of using content to demonstrate mastery of a skill

G2 = second generation family members, G3 = third generation, and so on…

Governance = a shared understanding for decision making, usually with written guidelines. Examples: The Dawsons had plenty of material wealth. But no governance. Like many Next Gen beneficiaries, they were anxious to discover the trust terms from Chamberlain. Then they quickly hired a triad of expert advisors- Dr. Jenn for process, Colton for finances, Jake Jr. for legal concerns. Those advisors may accelerate good governance, and smart decisions, for the siblings. Even for scary beneficiaries like the G&G, LLC.

Gratitude = the behavior of expressing appreciation for the good things in life

Growth mindset = a belief of openness to new ideas or behavior

Hope = the capacity to believe in the will and the way toward a desired outcome. Example: When Harper visits the shooting gallery, Big Mamas, she vents her anger by shooting at images of her husband, Jordan. Then she expresses hope for the meeting with Chamberlain.

Individual system = a description of how people integrate skills and talents into a uniquely meaningful life

Informal learning = the process of using available resources to develop a skill or competency

Innovation = a new idea applied using experiments

Leaders = people who influence the behavior of followers toward a positive vision. The core skill of effective leaders is public optimism. Examples: Will asserts himself inconsistently and needs to develop his leadership skills. Nora Lee and Harper need to develop their influence with their followers, Hannah and Jake Jr.

Learning journal = an individual or team reference documentwith key questions, definitions, and resources

Learningsystem = a description of how people adapt to new informationand fit into a unique family or business

Loss aversion = a cognitive bias that influences people to avoid any real or perceived loss

Managers = people who maximize the productivity of others. The core skill of effective managers is coaching.

Negative feedback =statements that describe undesired behaviors

Operationalbehaviors = the required behaviors from people who deliver a product or service

Optimism = the ability of individuals or teams to believe in a better future. Examples: When Will, Grady and Colton describe the preppers and G&G, everyone expresses fear. Then optimism. All three siblings call meetings and take optimistic actions.

Ownership system = a description of how owners assess and manage the long-term assets of a family or business

Passive owners = people with an interest in an asset but do not have voting shares

Perception of fairness = the shared belief that a fair policy serves the long-term best interests of the owners and rewards desired behaviors

Positive feedback = positive statements that reinforce desired behaviors

Positive regard = the deepest human yearning based on safety, connections and dignity

Positivity spirals = behavior thatencourages people to broaden their options and build solutions

Primogeniture = an ownership practice of providing harmony and continuity to the eldest son

Psychological capital(Psy Cap) = a personal or team development model which measures Hope, Efficacy, Resilience and Optimism. For convenience in this fictional novel the word “agency” was substituted for the academic word “efficacy.” Example: After Dr. Jenn introduces the concept, the siblings use those four words more frequently. They practice these four new skills, when using AI, learning about G&G, or protecting Mason.

Relationship conflict = a description of the interpersonal interactions with others, that often perpetuate negative behaviors

Resilience = the ability of individuals or groups to get through difficult times or circumstances. Example: When Nora Lee has another panic attack, and four people quickly support her.

Risk avoidance = the willingness to avoid one behavior

Risk tolerance = the willingness to do one behavior instead of losing another related behavior

Self-awareness = a personal narrative from assessments or feedback that should be reliable and valid

Self-deception = an inaccurate personal narrative based on low self-awareness or inaccurate feedback from others

Shareholder dynamics = the infinitely complex dynamic interactions between shareholders, each with a vested interest in real or potential assets

Social capital = a measure of the tangible and intangible relationships between people

Task conflict = a description of the information necessary to function with others

Triangulation = the communication practice of sharing information indirectly when it should be shared directly. Example: Every time one of the siblings asked, “Have you talked with our mother?” instead of finding Regan. Many families avoid direct communication. Just like the Dawson’s, triangulation perpetuates chaos.

Value-based consulting = a process designed to structure key relationships, results and personal behaviors

To discuss your Family Wealth Advisory concerns (e.g., succession planning, asset transfer, legacy, governance, philanthropy, communication…) or 360 leadership assessment consulting services, visit www.Action-Learning.com ASAP.

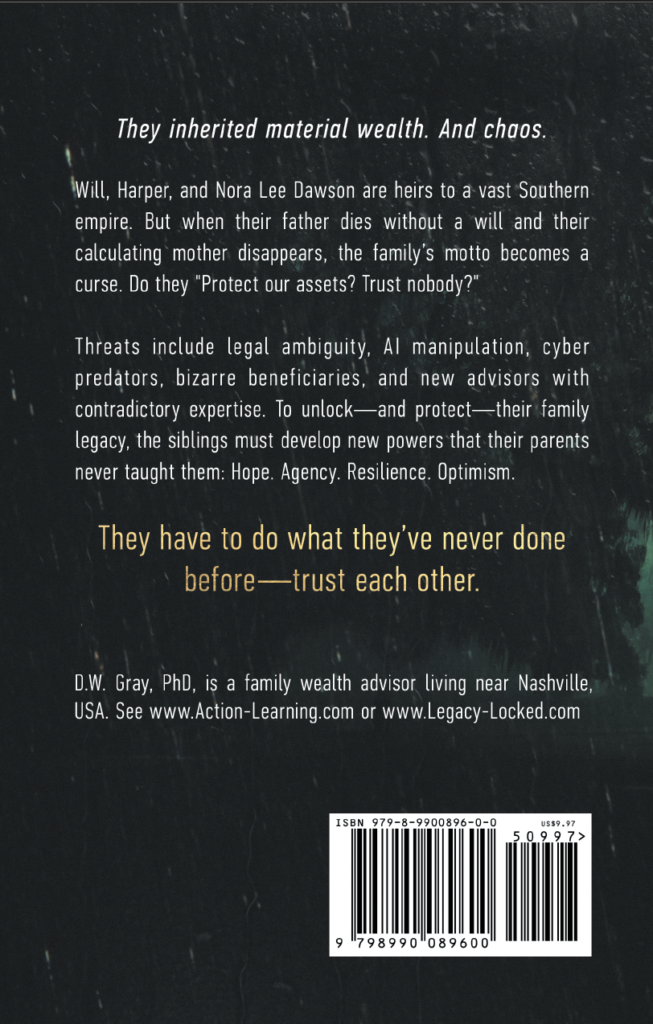

Will, Harper, and Nora Lee Dawson are heirs to a vast Southern empire. But when their father dies without a will and their calculating mother disappears, the family’s motto becomes a curse. Do they “Protect our assets? Trust nobody?”

Threats include legal ambiguity, AI manipulation, cyber predators, bizarre beneficiaries, and new advisors with contradictory expertise. To unlock – and protect- their family legacy, the siblings must develop new powers that their parents never taught them: Hope. Agency. Resilience. Optimism.

They have to do what they’ve never done before— trust each other.

FREE access is at https://action-learning.com/product/legacy-locked-book/. Use the coupon code crubne3q

Legacy Locked is more than a novel.

It’s a journey into the forces that shape what we inherit… and what we hide.

Gift #2: Download Legacy Locked book now. While it’s still free. FREE access is at https://action-learning.com/product/legacy-locked-book/. Use the coupon code crubne3q

Because the only thing scarier than a locked legacy… is never knowing what was inside.

Over decades of work with family business leaders, wealth advisors, and family office professionals, I see the same pattern. Failures result from too much dependence on financial and legal matters. People are emotional. Families are doubly emotional! Right? Think of your family or a client’s emotional mess. Yikes!

Those blind spots can be avoided. Most successful wealth transfers and succession plans occur when some third party expert facilitator supports the process- not the financial and legal factors.

The Missing Piece in Traditional Wealth Planning

While financial and legal expertise IS necessary, they are NOT sufficient. This insight comes from decades of observing what actually happens in family wealth transitions.

Traditional approaches to succession planning typically excel at the easy details that AI can now provide:

Creating tax-efficient structures

Drafting comprehensive legal documents

Developing sophisticated investment strategies

But owners and advisors frequently overlook critical components such as:

The psychological readiness for wealth responsibility – As I’ve written previously, “Next Gen leaders always question if they truly belong, especially if they joined through marriage or face complicated family dynamics. Many Next Gen leaders feel anxiety, loneliness, or self-doubt… and optimism.”

Family communication dynamics – In my experience, even the most brilliantly crafted estate plan fails when the family can’t effectively communicate about difficult topics. Someone is likely to say or do the wrong thing. Unless the process is expertly facilitated.

Leadership development beyond technical knowledge – As noted in my work with books, “Next Gen leaders need more than financial literacy. They need communication skills, emotional intelligence, and the ability to balance innovation with tradition.” Those are dynamic skills. Measurable skills. And very coachable skills!

Thoughtful technological integration – When technology serves human connections instead of replacing them, even the most traditional family members can become enthusiastic supporters.

The Kitchen Table Council Approach

In my article “Making AI Work for Family Businesses,” I described the concept of a “kitchen table council” where multiple generations come together to solve problems collaboratively. This approach exemplifies what effective wealth transition looks like in practice. It is bringing together different perspectives while respecting each voice.

This methodology addresses the full spectrum of challenges facing family enterprises, not just the financial and legal aspects but also the crucial human elements that ultimately determine success or failure. This approach tackles all challenges for family businesses, including financial, legal, and critical human factors impacting their success.

The Four Pillars of Our Legacy & Wealth Leadership Approach

Based on decades of work with family enterprises, our Legacy & Wealth Leadership approach addresses four essential dimensions:

1. Individual Coaching

Next-generation leaders face unique challenges in assuming wealth responsibility. Our coaching helps them develop:

Decision-making frameworks for complex situations

Communication skills for difficult conversations

Emotional intelligence to navigate family dynamics

Personal clarity about their role in the family legacy

Next Gen leaders particularly benefit from structured peer environments where Family and Non-Family Business leaders can share experiences, expert practices, and gain clarity.

2. Team & Family Facilitation

Even brilliant individuals falter without effective team dynamics. Our facilitation services help family enterprises:

Resolve communication breakdowns

Transform destructive conflict into productive dialogue

Align around shared values and vision

Develop governance structures that stand the test of time

In my experience, the power of an interdisciplinary team of advisors cannot be minimized. It’s hard for advisors to ‘sing from the same page’ as if huddled around one piece of paper, but we can do so! And the results can be a beautiful four-part harmony.

3. AI Strategy & Integration

Technology is transforming every industry. Our approach helps family businesses:

Identify the right technological opportunities for their unique situation

For the past year, I’ve focused on how AI can accelerate leadership development. In speeches and product demos clients have practiced difficult communication skills. One client went to www.JITCoach.com and selected role plays and avatars, then practiced 14 times before her next family meeting. The implications are profound for any individual or team leaders who are committed to professional development.

4. Family Office Structuring

For more complex family enterprises, comprehensive wealth structures are essential. Our family solutions help:

Design integrated governance systems

Create communication protocols that strengthen family bonds

Develop decision frameworks that balance innovation with tradition

One of the most influential thinkers alive today is XPrize founder and MD, Peter Diamandis… [who shared] “It is not the strongest of the species that survives, nor the most intelligent that survives. It is the one that is most adaptable to change.” I wrote about those changes for Family Business Consulting in the International best seller,

Why 2025 Demands New Action

The coming months represent a critical period for family enterprises for several reasons:

Technological transformation is accelerating at unprecedented rates

Economic uncertainty accelerates both risks and opportunities

Generational expectations continue to diversify

The pace of wealth transfer is increasing as Baby Boomers age

Families who address these challenges holistically will not only preserve their wealth—they’ll strengthen the bonds that give that wealth meaning.Families who comprehensively tackle these issues will safeguard their wealth and reinforce the relationships that make it valuable.

Join Me for a Virtual Open House: Legacy & Wealth Leadership

If you’re responsible for family wealth—whether as an owner, Next Generation leader, or advisor—I invite you to join me for a virtual event where we’ll explore these topics in depth.

On May 22nd at 11am ET, I’m hosting a short “Legacy & Wealth Leadership” Virtual Open House. You’ll learn:

Why traditional approaches to wealth transition often fall short

Our integrated methodology addressing human dynamics alongside financial structures

Real outcomes in both family harmony and financial returns

As I often tell my clients, “Smart leaders don’t wait for the perfect moment… because they understand there is no perfect moment.” The time to address these critical family wealth challenges is now.

With so much noise surrounding artificial intelligence these days, it’s easy for leaders to feel overwhelmed. Is AI just another tech fad, or is there genuine value beneath the buzzwords? In this conversation, we explore how AI has rapidly evolved from a novelty into an essential business tool and why family businesses are uniquely positioned to benefit from its practical applications.

The Technology Adoption Lifecycle

Think about where Siri and Alexa were just a decade ago. People found them odd and creepy, resisting the idea of being recorded or having their preferences tracked. Fast forward to today, and these AI assistants have become so integrated into our daily lives that we interact with them as if they’re another person in the room.

The technology adoption lifecycle follows a predictable pattern. We’ve moved beyond the innovators and early adopters phase of the 1990s and are now firmly in the early majority phase, where 34% of users are seeking pragmatic use cases. We know AI works, just like Siri and Alexa work. People are using ChatGPT regularly because it’s faster, more reliable, cheaper, and can be confidential.

And who makes the best users? Small business owners and family businesses. They’re agile and adaptive, without the compliance requirements and legal teams that might say “no” in larger organizations. They’re curious about how AI can benefit their businesses.

How Families and Small Businesses Can Cut Through the AI Noise

For leaders feeling overwhelmed by AI hype with countless platforms being thrown at them daily, it’s understandable to feel a sense of AI fatigue. Rather than trying to figure out everything at once, it’s more effective to focus on specific problems you’re facing and then explore how AI might help.

Let’s take sales as an example. A two-year cross-industry study found that sales teams using AI-powered training sold 24% more than teams that didn’t. Most companies would go to extraordinary lengths for even an 8% increase in revenue. This represents a simple, cost-effective tool that eliminates the risk of salespeople learning on the job with real clients. They can safely master all personas, objections, and value propositions before stepping into the field.

Overcoming Fear and Resistance to AI Adoption

Fear often defines us. Whether it’s fear of geopolitical decisions, new technologies, or change in general, we naturally resist what we don’t understand. But when evaluating any new technology, we should consider three key factors: Is it efficient? Is it effective? And what are the outcomes?

Every specialized profession is facing disruption right now:

Attorneys may resist robo-advisors

Wealth investors might shy away from AI-driven investment strategies

Organizational employees might fear automation replacing human roles

Yet every industry will be affected by AI in direct ways within the next 5-10 years. So why not overcome that resistance and learn how to implement AI in your business?

When faced with change, we typically respond in one of three ways: freeze, flight, or fight. We can freeze like a rabbit in the forest and try to ignore AI’s inevitable adoption. We can run away from it. Or we can fight—not against AI, but alongside it, wrestling with its potential until we master it.

If 45% of business owners are already using AI and your competitors are among them, the question becomes: why wouldn’t you use it now, especially if you had a secure way to do so in a closed system?

The Human Element: Why a Hybrid Approach to AI Coaching Matters

While AI platforms like Claude can help draft emails or prepare for difficult conversations, they lack the human dimension that addresses the emotional challenges we face. What if you could combine AI with human coaching to improve your ability to handle difficult and sensitive conversations?

Imagine practicing a difficult conversation with an AI avatar programmed to respond like the actual person you’ll be speaking with. As you rehearse multiple times, your confidence grows. Then, when you discuss your progress with a human coach who can address your internal struggles and provide personalized feedback, you’re getting the best of both worlds.

This hybrid coaching approach is three-dimensional rather than flat. The AI component provides consistent practice opportunities and immediate feedback, while the human coach adds depth, emotional intelligence, and personalized guidance that helps the learning stick.

Communication capability makes a tremendous difference in business success. Strong communication skills in leaders allows them to put out “people fires,” handle employee conflicts, reduce turnover, and free up business owners to focus on leadership and maintain work-life balance.

Effective management hinges on the ability to have productive conversations around delegation, feedback, accountability, hiring, termination, and performance improvement. Developing these skills traditionally required significant time investment from the manager and trainee. Now, with AI-assisted practice, managers can rapidly develop these crucial skills through repeated role-plays and targeted feedback.

Another study showed that this approach improved management capability by 24%. For small business owners struggling with operational challenges, this represents a fast, cost-effective way to make significant improvements.

Getting Started with AI

For those excited about AI and already using various platforms, the key is to just begin. Experiment and dabble. Pick any platform—ChatGPT, Perplexity, Claude, Poe—and start using it. The paid options ($20/month) generally provide better results.

If you have digital content—books, research, business documents—you can upload them to create a personalized AI that speaks your language. And by selecting privacy options that prevent sharing your content with large language models, you’ve created a confidential AI system for your organization that nobody else can access.

Many businesses are already using these tools for business protocols, operational processes, manufacturing, and marketing analyses. The question isn’t whether to adopt AI, but why wait any longer?

The future of professional development isn’t just AI or just human coaching—it’s both working together to accelerate your growth and success.

This blog post was adapted from a conversation with Doug Gray and Israel Hillegeist on practical AI applications for small businesses.

Interested in learning more about AI Coaching for Communication? Join the next edition of the Next Gen Leadership Series. https://www.nextgenpeergroups.com/the-next-gen-leadership-series

We wrote this conversation based on a short video recording… edited by AI tools that summarized us. Then edited by our marketing manager, Erin, who is a real person. We imagine that any leader, in any sector, can learn how to use AI in their business immediately. Reply or comment or connect?…. see www.JITCoach.com or schedule a demo

Artificial intelligence dominates headlines with promises of revolutionary change, so it’s easy to feel overwhelmed by the noise. But beneath the hype and buzzwords lies tremendous value that can be applied immediately—particularly for family business leaders, Next Gens and smaller organizations.

Cutting Through the AI Noise

There’s a lot of “hoo-ha” around artificial intelligence today. Open any business publication—Harvard Business Review, McKinsey reports, VentureBeat, or Forbes—and you’ll find endless articles about AI’s utility, examples, and trends. Terms like “predictive analytics” get tossed around without clear definitions. Can we truly predict the next word in a sentence or the next market opportunity? There are tools like Lex Machina and Bloomberg Law that can forecast divorce or succession risk. But should they do so? The ethical clarity isn’t always there.

What we call “artificial human intelligence” are essentially algorithms—compilations designed to anticipate the next word. You’ve experienced this already: when you type “How do I…” into a Google browser, it fills in the likely next words, based on your search history. This predictive capability has evolved from simple sentence search completion to sophisticated tools like Microsoft’s Copilot that can generate content, edit documents, and create personalized interactions. AI learns from itself, which is why the default browser for Google has recently been replaced by Gemini.

The Rise of Customized AI

One of the most powerful developments is the ability to create customized AI systems. I’ve built what some call a “closed chat GPT”—an AI trained on my books, dissertation, research papers, blog posts, and website content. I call it “Gray Matters” and share it with my clients. When asked, “How would Doug respond to this situation?” it provides evidence-based answers drawn from that data set. Crucially, you can configure these closed systems to maintain confidentiality, which prevents your data from being shared with large language models.

Small business leaders can leverage this same technology. If you need to maintain client confidentiality for legal reasons but want to provide unique value to those clients, a closed AI system offers a perfect solution. This fact explains why there are so many chatbots on company websites—they’re cost-efficient and can provide consistent service 24/7. Do you need to invest in Schwab or Fidelity or Vanguard? Then you need to interact with bots before humans.

Digital Trust and Consumer Adaptation

Remember when Amazon first introduced Prime? Many doubted that package would succeed. Now one-click purchasing and “people like you bought” suggestions have become standard AI tools. These weren’t implemented randomly—they were based on extensive data analysis showing that buyers of one product were likely to purchase related items.

This example reflects a broader trend: we have developed increased digital trust in AI tools. Think about how you interact with Siri or Alexa—as if there’s another person in the room. These AI assistants weren’t part of our lives a decade ago, yet now they’ve become integral to our daily routines. Our expectations around AI are also shifting—we expect it to be personalized, always available, and worthy of our digital trust.

Accelerating Leadership Development

For the past year, I’ve focused on how AI can accelerate leadership development. The implications are profound for any individual or team committed to professional development. We can now provide 24/7 utility to confidential resources and interactive learning opportunities using AI avatars based on customized role-plays and scenarios.

Imagine clicking on ChatGPT repeatedly to gain insight into difficult topics: How do I deal with anxiety? How do I sleep better? How do I have a difficult conversation with a family member who’s resistant to dialogue? Now, these are skills that can be developed through deliberate practice.

Years ago, when I asked Google, “Can you be my executive coach?” it said “Not at this time.” Today, any AI platform—whether it’s ChatGPT, Claude, Grok, Poe, or another—will happily take on that role.

Our Hybrid Coaching Solution

AI can re-design executive coaching, leadership consulting, and transform your career. Imagine using hybrid coaching that combines AI practice with human expertise. Let me give you some examples.

A client named George wanted to develop better communication skills but didn’t want to ask his manager for help. Using our AI platform, George practiced difficult conversations repeatedly in a confidential environment. Then, when we meet for our 1:1 executive coaching session, George can share his screen and show me his AI interactions. I can provide feedback not just on the content of his responses but on his approach to learning.

This hybrid model works across professions. Imagine you’re a lawyer with clients who need to discuss succession planning, or a family wealth advisor helping clients prepare for difficult conversations with the next generation. These discussions require skills that many people haven’t developed. Behavioral feedback can provide better analysis and coaching suggestions than humans. When we practice new skills with AI, my clients can find the right words and approaches before having those crucial real-world conversations.

B2C and B2B Applications

I’ve developed two models for implementing hybrid consulting:

B2C (Business to Consumer): Individuals can access a platform to practice scenarios like dealing with anxiety, burnout, difficult family members, or deeper questions about purpose and faith. For about $100 monthly ($1,200 annually), users get unlimited access to AI-assisted practice scenarios. That investment often delivers more lasting value than a couple of traditional coaching sessions at the same investment level. See www.JITCoach.com or ask for a demo.

B2B (Business to Business): Teams and organizations can implement AI-assisted consulting to accelerate skill development. The data is compelling—sales teams using these approaches have shown a 24% increase in sales performance and 97% improvements in training retention. Compared to traditional online training programs that often show minimal results, this AI-assisted consulting represents a breakthrough. See www.Action-Learning.com or ask for a demo.

The Bottom Line

Artificial intelligence has been evolving since 1995. Now we have reached a point where it’s more consumer-friendly and accessible than ever. Just as you talk to Siri or use ChatGPT, you can now use AI-assisted consulting tools to accelerate your skill development, improve communication, and achieve outcomes faster, more effectively, and more affordably.

We will interact with AI-driven cars and live in an AI-enhanced world. Why wouldn’t we apply these same technologies to leadership development and executive coaching?

Want to learn more about implementing AI in your leadership development? Contact Doug at doug@action-learning.com or visit action-learning.com to schedule a demo.

Recent Comments